Despite being in a holding pattern for about a year, the California Privacy Protection Agency (CPPA) is now poised to enforce the CPRA without further delay. Michael Macko, deputy director for enforcement for the CPPA, emphasized their readiness to begin enforcement, stating, “We are pleased that the court has restored our full enforcement authority, and our enforcement team stands ready to take it from here.”

Here is a short excerpt of some of the CPRA’s most salient points. We will discuss these issues, and others, at length in a future article.

“Sharing” included in all “selling” requirements regarding personal information: “Sharing” occurs when a consumer’s personal information is disclosed to a third party for cross-context behavioral advertising whether or not for money or valuable consideration. The right to opt-out now includes “sharing.”

Consumer correction of inaccurate information: Consumers now have the right to request that a dealer correct inaccurate information about them. Not only will the dealer have to do this, but they will have to notify all downstream Service Providers of any corrections.

Foreign language translations of privacy policies and DSAR: All CCPA/CPRA disclosures must be translated into foreign languages commonly used at the dealership. This includes online components, including cookie banners, privacy policies, and data subject access request (DSAR) portals.

Standardized opt-out signals: Dealers must now honor all standardized opt-out signals in addition to Global Privacy Controls (GPC), such as “Do Not Track” signals. New disclosures must notify the consumer that the various signals have been honored.

Opt-out of specific use of “sensitive information”: Consumers now have the right to opt-out of the use and disclosure of certain categories of “sensitive information” for the purpose of inferring characteristics about consumers. For example, geo-targeting and geofencing can give precise geolocation data that businesses can use to infer whether someone has shopped at a competitor or where they live.

Addendum with all “third parties” AND “service providers”: Dealers must now have both third parties AND service providers complete an addendum that outlines how they use the personal information that they collect.”

“Dark pattern” designs prohibited: “Dark patterns” are instances where functionality is designed to trick or manipulate the user either to encourage or discourage certain behavior. In an effort to curb “dark patterns” as it relates to sharing personal data, the CPRA puts in place design parameters around the cookie banner and DSAR portal to make it clearer for consumers to exercise their rights. A prime example are symmetrical “accept” and “decline” buttons for opt-out purposes.

Alternative Opt-Out Link: In lieu of a “Do Not Sell or Share My Personal Information” link, dealers may now use an alternative opt-out link. The link must be titled “Your Privacy Choices” or “Your California Privacy Choices” and include the following icon:

Note that this alert is intended for educational purposes only and is not legal advice. If you require legal advice, contact competent counsel. If you have more questions, please call CNCDA’s Legal Hotline at (916) 441-2599.

New Employment Policies and Documents for 2024

Downloadable at the link above is a PDF that includes various items related to the topics discussed in the California New Car Dealers New Laws Seminars for 2024.

The following documents include the following new/updated policies:

Paid Sick Leave/PTO (combined plan to replace existing Paid Sick Leave and Paid Vacation policies)

Alcohol and Drug Policy

Reproductive Loss Leave

Off the Clock Work Prohibited

Uniforms and Laundry

Confidentiality Agreement for New Hires

Confidentiality Policy for Employee Handbook

Because these are sample policies, you should always seek the advice of competent employment lawyers in the auto industry to make sure your particular operation meets the requirements to use the policies attached hereto as written, as sometimes we find that dealerships have different approaches to certain human resources issues. Aa a result some modifications must be made to these policies and those changes should be identified and drafted by competent legal counsel.

COMPLYING WITH SB 55- FREQUENTLY ASKED QUESTIONS- 12.18.23

What options do I have to comply with SB 55?

At the highest level, dealers have two options to comply with SB 55:

Option 1:The dealer marks the VIN on the catalytic converter prior to the sale and advertises the price of the vehicle, including any cost for the marking. In this option, catalytic converter marking would be treated in the same manner as any other additional pre-sale dealer-installed equipment (such as a tow hitch).

In either a cash or finance sale, a dealer should obtain the customer’s signed acknowledgment in the event the customer declines the catalytic converter marking. CNCDA’s 2023 Legislative Summary discusses this requirement in greater detail, and a question below discusses how a dealer can obtain the customer’s declination using a new form from Reynolds & Reynolds.

May I select different options (options 1 and 2, above) for different vehicles on my lot?

Yes. A dealer could choose to mark certain vehicles prior to sale and offer catalytic converter marking as an optional product for other vehicles. For example, a dealer may find that it is relatively easy to mark many new vehicles during the PDI process and choose option 1 (see above) for those vehicles. A dealer could select option 2 (see above) for vehicles where marking is more complex or difficult and identify a reasonable price for the optional product that reflects the complexity of the task.

Can I mark a unique identification number instead of the VIN?

No. The law requires dealers to mark the VIN. VIN marking was important for supporters of SB 55, as the VIN can be accessed more directly by law enforcement.

I’m offering catalytic converter marking as an optional product. Is there a form available to record a customer’s declination when they don’t want the vehicle marked? Yes. Available now from Reynolds & Reynolds, the LAWCA-CAT-DCL and LAWCA-CAT-DCLF forms allow a dealer to record the buyer’s declination. Both forms comply with California law, but the “DCLF” version of the form includes a field for the dealer to include the offered price of the marking of the catalytic converter. California law does not expressly require dealers to include the price in the form, but it is seen by some dealer counsel as a best practice.

I’m offering catalytic converter marking as an optional product. Can I bundle the catalytic converter marking with a warranty product that covers the theft of the catalytic converter?

CNCDA recommends against bundling any warranty products with the marking of catalytic converters unless you consult competent counsel before doing so. There are several reasons for this. First, it’s unclear if a dealer would be excused from its obligation to mark a catalytic converter if the customer declines the marking of a product that is bundled with a warranty.

Second, the sale of a warranty on a catalytic converter may constitute the sale of insurance under California law, which triggers licensure requirements and regulation by the California Department of Insurance. As such, dealers are strongly encouraged to contact competent counsel before offering warranties on catalytic converters.

I’m offering catalytic converter marking as an optional product. If a customer selects the option to purchase catalytic converter marking, can I deliver the vehicle to the customer and create a ‘due bill’ that instructs the customer to return later to have the catalytic converter marked?

If a customer does not decline the option to mark the catalytic converter, SB 55 requires the dealer to mark the catalytic converter prior to sale. If a customer wants immediate delivery of the vehicle and wants the catalytic converter marked, and the dealer is unable to mark the catalytic converter immediately, the customer could opt-out of the marking at the time of sale and return the vehicle later to have it marked. In this situation, the customer would sign the declination form indicating that they don’t want the vehicle marked at the time of sale, and any cost for the catalytic converter marking would not be included in the sales contract and instead be noted in a separate invoice at the time the customer returns to have the catalytic converter marked.

Some of my vehicles have more than one catalytic converter. Do they all need to be marked?

Yes. CNCDA recommends that all catalytic converters be marked unless the marking is offered as an optional product and the customer opts out.

Some of my vehicles require substantial disassembly to mark the catalytic converter(s). Do I still need to mark the vehicle?

Yes (unless you are offering the marking as an optional product and the customer declines the marking). That said, the law does not limit your ability to adjust the price of the product based on the complexity of the operation. In other words, if it is time-consuming or expensive for you to mark a hard-to-access converter, nothing prevents a dealer from passing along that higher cost to the customer.

Does SB 55 apply to wholesale transactions?

Generally, SB 55 applies to wholesale transactions that do not occur through an auction. In other words, dealers need to either mark catalytic converters prior to non-auction wholesale transactions or offer catalytic converter marking to wholesale customers and obtain their declination.

More specifically, SB 55 contains an exception for wholesale transactions that occur “by or through a wholesale motor vehicle auction” where the dealer that is conducting the auction does not take ownership of the vehicle and the vehicle is sold to a nonretail buyer for resale. This should cover typical wholesales that occur through an auction, but dealers that have concerns about specific transactions should contact the relevant auction company or competent counsel.

Where should I mark the catalytic converter? May I mark the heat shield instead of the converter itself?

SB 55 requires the marking to be on the catalytic converter, not a related component like the heat shield. Beyond requiring placement on the catalytic converter, SB 55 does not specify where the marking should be placed. Dealers should use their best judgment in the placement of the marking to reliability and permanently mark the entire VIN on the catalytic converter.

Does SB 55 limit the ability of a dealer to price catalytic converter marking?

The bill does not address how a dealer may price the product, beyond requiring catalytic converter marking to be disclosed as a “theft deterrent device” in the event the dealer offers the service as an optional product. The legislature anticipated that dealers would likely pass this cost onto consumers, and that the price of the marking would vary based on the difficulty to mark a vehicle. Moreover, the legislature contemplated that the price of catalytic converter marking for difficult-to-mark vehicles may deter customers from purchasing catalytic converter marking for such vehicles. The Senate Rules Committee analysis on SB 55 notes: “By allowing dealers to either etch a converter or offer consumers the option to reject etching, this bill promotes converter etching for easy-to-access converters and allows consumers to decide if the cost of etching hard-to-access converters is worth the theft prevention and prosecution aid VIN etching may provide.”

Note that this alert is intended for educational purposes only and is not legal advice. If you require legal advice, contact competent counsel. If you have more questions, please call CNCDA’s Legal Hotline at (916) 441-2599.

Memo on Credit Card Surcharges

Over the past couple of years, we’ve received an increasing number of inquiries from dealers about whether they can impose credit card surcharges at their stores. To aid your dealership in developing an appropriate policy, CNCDA is providing our members a detailed legal memorandum on credit card surcharges, which is available on CNCDA Comply.

Fixed ops (service/parts sales) – credit card surcharges may be imposed, provided that they are clearly and conspicuously disclosed to the consumer on the receipt/invoice and by signage displayed at the cash register.

Installment sales/lease contracts – credit card surcharges occupy a legal grey area, and dealers should closely review the memo’s findings with their counsel to implement an appropriate policy.

Cash sales – credit card surcharges may be imposed, provided that such surcharges are clearly and conspicuously disclosed.

The memo is available on CNCDA Comply by clicking on the link above.

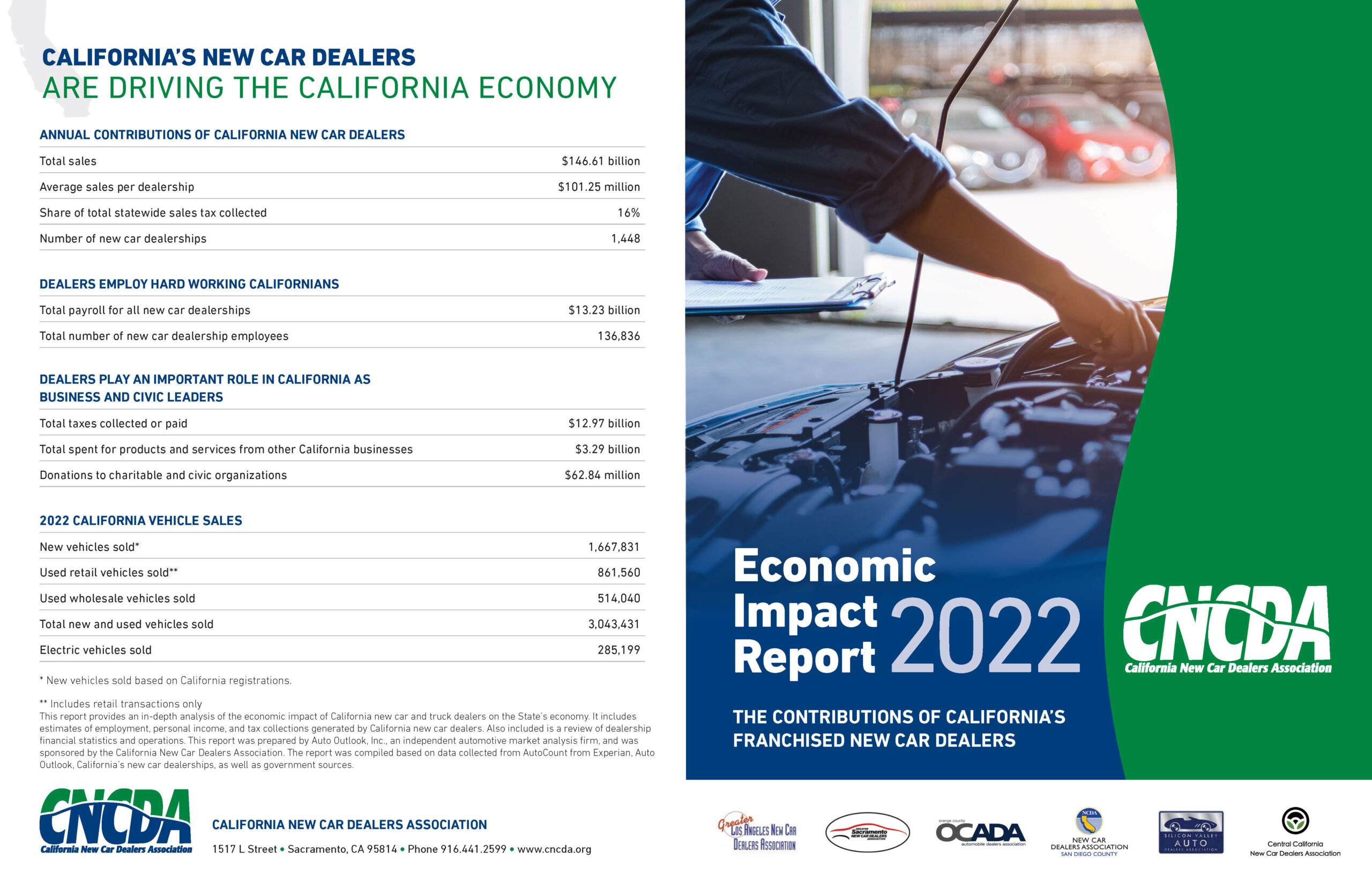

2022 Economic Impact Report

Click on the image below to view the full report.

Federal EV Tax Credit Forms

The new clean vehicle tax credit applies to clean vehicles placed in service after January 1, 2023, and acquired by a taxpayer for original use. To qualify for the credit, the vehicle and the consumer must meet certain requirements. To view those requirements and a list of qualifying vehicles, click here. The site will be updated as more vehicles are added to the list. Importantly, the seller of a new clean vehicle must provide a report containing taxpayer and vehicle information to the taxpayer and to the IRS for the consumer to receive the credit. These reports will need to be compiled and filed with the IRS by January 15, 2024. Click here for more details about the form. NADA has created a model sellers report form for this purpose, linked below.

In addition to the new clean vehicle tax credit, there is a previously owned clean vehicle tax credit available. Click here to view eligibility details. Dealers must also provide a report to taxpayers/purchasers upon sale of a previously owned vehicle potentially eligible for the Section 25E Previously Owned Clean Vehicle Tax Credit. NADA has created a model sellers report form for the 2023 IRC Section 25E previously owned clean vehicle tax credit, linked below.

On December 30, the U.S. Department of Treasury, in conjunction with the IRS, released preliminary guidance indicating consumer leases qualify for the commercial clean vehicle credit under 26 USCS § 45W. Effectively, this guidance removes much of the vehicle sourcing and income requirements from consumer lease transactions. However, these vehicles will still be subject to the commercial clean vehicle credit requirements, and it is important to note that retail vehicle sales are still subject to the § 30D requirements. Click here to view the guidance fact sheet.

While Treasury and the IRS often allow taxpayers to rely on proposed guidance in the interim between notice and issuance of regulations, it is important to note that this guidance is not regulatory action, and dealers should stay tuned as CNCDA and NADA follow this developing body of law. We also encourage dealers to access and review the materials prepared by NADA, available here.

Voluntary Protection Products Policy – Template for California Dealerships

This sample employment arbitration agreement (available in English and Spanish language) has been developed by Fine, Boggs, & Perkins for CNCDA members. It is current as of May 9, 2022. Consult competent counsel prior to implementing any changes to your dealership’s employment policies or practices.

CNCDA commissioned a legal white paper by preeminent experts at the Munger, Tolles & Olson LLP law firm on the use of e-signatures for vehicle sales and lease contracts in California. The chief author of the memo – Donald Verrilli – is one of the nation’s premier Supreme Court and appellate advocates. He served as Solicitor General of the United States from June 2011 to June 2016 for the Obama Administration.

The white paper unambiguously concludes that “the use of electronic signatures and records in connection with the sale and leasing of automobiles is lawful in California.” You can download it by clicking on “Download PDF” above.

The white paper’s conclusion is supported by recent statements by the California DMV Director on the use of electronic signatures for vehicle purchases. Following the DMV’s approval of electronic submission of odometer statements, Director Gordan proclaimed: “Buyers can now complete their purchase from anywhere – no ink or paper required.” Click here to read more.

CNCDA understands that some dealers are hesitant to adopt the use of electronic signatures for vehicle sales and lease transactions, as such transactions are not expressly authorized by the California Uniform Electronic Transactions Act (CalUETA). CNCDA sought to provide clarity on this issue by introducing legislation to amend CalUETA in 2021. However, our bill was blocked by trial attorneys and other special interest groups, who sought to use our bill as leverage to impose additional onerous restrictions on dealers.

If you have hesitated to adopt the use of electronic signatures at your dealership, please review the attached white paper with your counsel, as we believe it provides a strong basis to move forward with a fully electronicprocess at your dealership.